5 tips on how to empower your kids to fight today’s most insidious fraud type

The nightmare started for my friend Kathy when she checked the transactions on her banking app the day of Thanksgiving. Instead of going shopping for Black Friday deals, she spent the day dealing with a shocking surprise: her son’s checking account was overdrawn by $4,000. As it turns out, her son, who is 18 and regularly used the checking account she set up for him at age 13, had fallen victim to a romance scam on a dating app. At the request of a new love interest, the young man had deposited multiple checks through his mobile banking app and quickly transferred the funds out, before the checks were returned and deducted from his balance.

The nightmare started for my friend Kathy when she checked the transactions on her banking app the day of Thanksgiving. Instead of going shopping for Black Friday deals, she spent the day dealing with a shocking surprise: her son’s checking account was overdrawn by $4,000. As it turns out, her son, who is 18 and regularly used the checking account she set up for him at age 13, had fallen victim to a romance scam on a dating app. At the request of a new love interest, the young man had deposited multiple checks through his mobile banking app and quickly transferred the funds out, before the checks were returned and deducted from his balance.

We are unfortunately all too familiar with how the rest of the story goes, and it is never a happy ending—the checks and the new paramour were fake. But the damage was very, very real. Kathy ended up having to pay back her bank almost all of the money because her son “knowingly” deposited these checks. She was surprised not just by his gullibility; as the owner of her son’s account, Kathy’s accounts and financial well-being were vulnerable to scammers, despite her son being an adult.

This blog, the first in a three-part series, provides an overview of check fraud and five tips on how you can talk with your kids in a simple and easy way that can help protect them, avoiding these painful situations. Part 2 explains how parents can protect themselves from check fraud perpetrated against their minor and adult children, and what you can expect as the responsible party if, despite your best prevention efforts, your child becomes a victim of check fraud. Finally, Part 3 is for readers who care for their parents or other elders; while most check fraud targeting teens occurs digitally, the elderly are more susceptible to scams involving paper checks.

What parents need to know

Kathy’s son was not alone; the amount of money lost to scammers by people ages 20 and younger grew nearly 2,500% in the last five years. Check fraud is an increasingly popular choice for financial criminals targeting teens; they creep into kids’ digital lives and then vanish. Check fraudsters exploit the teen demographic’s relative unfamiliarity with this payment type, quickly extracting maximum funds against illicit deposits through a combination of Zelle instant payments and apps such as CashApp and ApplePay, which offer recipients immediate in-app availability of funds transferred to them. Kids over 13 can use CashApp, for example, “sponsored by a parent or trusted adult,” but many minors get accounts without parental knowledge.

If you’re a parent of any child under 18 with a smartphone, they are potential targets for scammers trolling social media apps like TikTok, Snapchat and Instagram, gaming apps, dating apps (many teens are on these despite the apps requiring users to be 18) and any online destination where young people gather. Here’s what you need to know to protect your kids and your own finances:

- You will almost certainly be held financially liable for damages stemming from check fraud in these instances. The implications of check fraud for you as a parent range in severity, depending on the situation. But at the end of the day, if your child 18 or older and still using the same bank account you opened for them when they were a minor, you may be held liable. The parent is the legal custodian of that account for as long as it remains open, unless ownership is transferred by the child to their own name after they turn 18.

For this reason, you should have your child transfer their account to their ownership and take you off as soon as reasonably possible after they turn 18. This is not so much to protect you from legal liability for their actions, but to keep thieves from automatically accessing your linked account if check fraud overdrafts pile up on your child’s account. - Check deposit fraud is handled by banks differently than credit card fraud. Many of us have experienced credit card fraud, and resolving it with our banks usually has no financial impact if reported in a timely fashion. But check fraud regulations are different than those for credit card fraud. Consumers need to be aware of the differences and what protections they have, as well as what their bank’s policies are in their deposit agreements. In the case of Kathy’s son and similar scams (such as authorized push payment fraud), check fraud is perpetrated “knowingly,” if unwittingly, by the account holder is not covered by fraud protections.

- Most kids today don’t receive a basic financial education at school—but you can use your bank’s tools to protect your accounts, and teach your children how to use them, too. Which brings me to …

5 tips on how to empower your kids to fight check fraud

- Monitor transactions: Use your banking app’s text alert features to notify you of any transactions over a certain threshold, such as $50, across the accounts you control, including your minor children’s. Teach your kids, with examples, why it’s a good practice to monitor transactions: to be made aware immediately of any unusual or unauthorized activity. Kathy was not using alerts, which allowed her son’s bad check deposits and transfers to “fly under the radar”—until it was too late.

- Help your child gain financial acumen: Use your checkbook as a teaching aid to explain how to write a check, how checks and deposits work, what a bad check is, and how fraudsters can get away with their crimes by taking advantage of funds availability regulations, cleaning out ill-deposited funds before the bank finds out the check was fake.

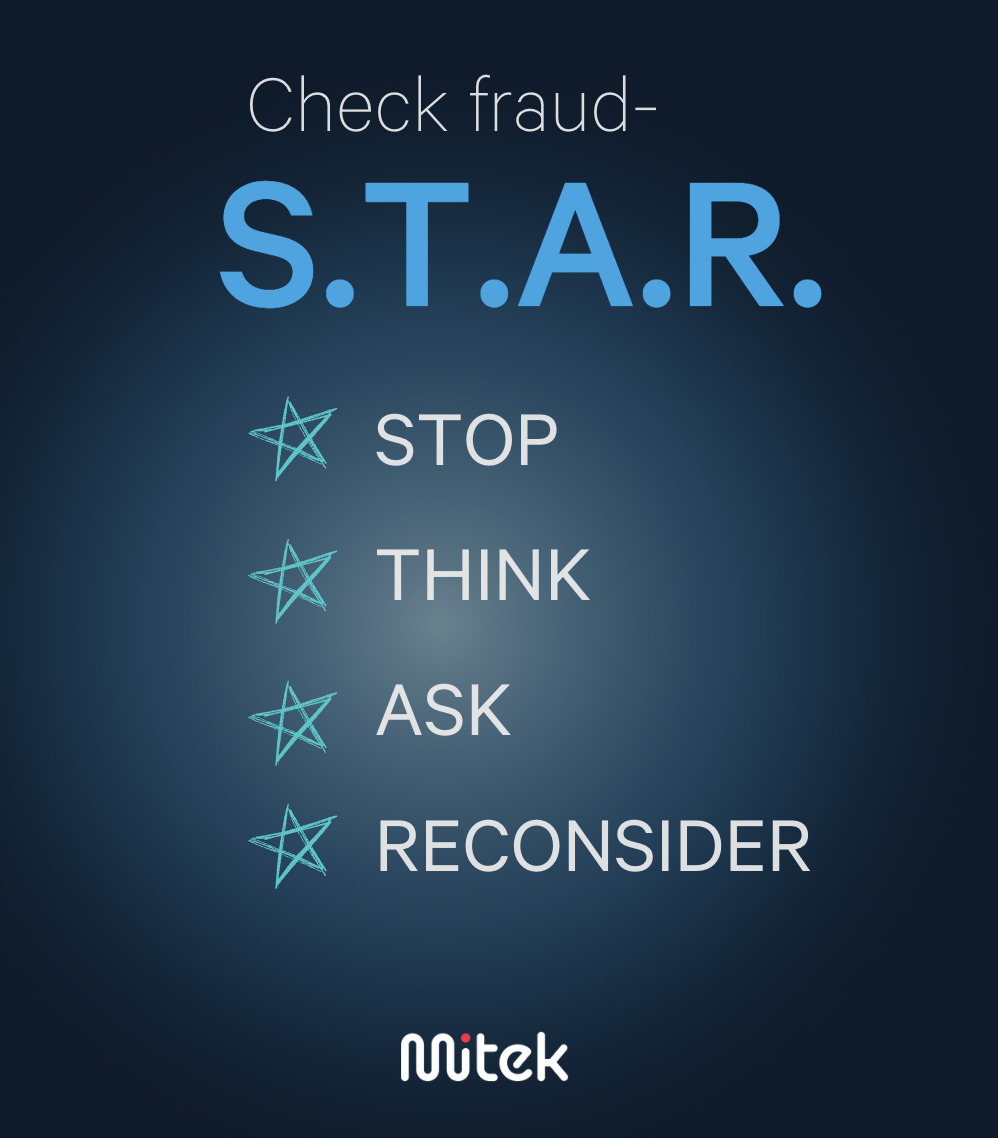

- Be a STAR: If your child is asked to deposit a check, work with them to develop a safe “STAR” reflex:

Stop: Don’t immediately follow through on the request to deposit the check—even if the person seems desperate or is pressuring you. Stop for a moment; fraudsters rely on feelings, not facts, to perpetrate check all scams, including check fraud.

Stop: Don’t immediately follow through on the request to deposit the check—even if the person seems desperate or is pressuring you. Stop for a moment; fraudsters rely on feelings, not facts, to perpetrate check all scams, including check fraud.- Think: Remember that when your deposit a check, you personally assume responsibility that it is genuine and backed by legitimate funds. If you’re unsure, don’t do it.

- Ask: Who is the person asking you to deposit a check? Do you know them in real life (IRL)? Is the person a stranger? Do your friends know who this person is? Do a quick online search to further check them out. If no one knows them IRL, and they don’t have a digital footprint, the stranger is not who they say they are.

- Reconsider: In life, many things that seem too good to be true often are. A stranger offering you hundreds or thousands of dollars for free, in exchange for a simple deposit and money transfer, is always too good to be true—no matter how nice they seem, or how badly they say they need you to help them, or how attractive the offer.

- Get in the habit of using your bank’s defenses: Work with your child to develop financial acumen; make it a habit to check their account every day to make sure all of the transactions are legitimate. Show your child how to set up alerts—it’s not only a good protection against fraud. Alerts help to monitor spending in real time.

Also, whenever possible, pay with a credit card, not a debit card, to take advantage of the fraud protection that credit cards offer to customers. Each payment method that can be used –check, credit card, ACH, and wire–– has their purposes; be attuned to which payment type is most secure for the transaction you are making. - Keep communication channels open: Talk with your kids openly about financial crimes such as check fraud. Let them know they can come to you with questions or problems, without judgment—“if you see something, say something.” Let them know they should talk about check fraud and scams with their friends and peers; they will undoubtedly learn that someone they know has been a victim of check fraud or other scams, which makes the threat that much more real.

In sum, by using your bank’s tools as a front-line defense, while educating your children on safe, responsible financial behaviors, you can protect both your kids’ well-being and your own finances. In my next blog, I’ll dive into what you as a parent can do to protect yourself from check fraud perpetrated against your minor children, what happens with your bank if your child does become a victim, and the steps you should take.

Follow me on LinkedIn to keep up with my latest thoughts on check fraud and how to fight it. You’ll be glad you did.

Check out Kerry's industry insights

Kerry Cantley — VP, Digital Banking Strategy at Mitek

Kerry Cantley is VP of Digital Banking Strategy at Mitek, leading the strategic expansion of Mitek’s Check Fraud Defender service, which detects forgeries and fraudulent activity across all deposit channels, otherwise missed by traditional fraud prevention protocols.